The wine of Bordeaux is inextricably tied up with its long history, the story of which is still being told decades after a vintage. On a Wednesday evening in April I was delighted to be included at a dinner at Domaine de Chevalier where some twenty of us, amongst whom were some proprietors from nearby Chateaux, enjoyed an excellent dinner which featured some extraordinary wines generously provided by our host and his neighbours. The star wine of the evening, perhaps not coincidentally, was a 1929 Domaine de Chevalier. It was as if the past had returned to haunt us, a reminder from a witness to the events of the time. Whilst the financial world collapsed, not dissimilarly to today, a wine was made whose destiny was fulfilled at our dinner table that night, almost eighty years later. It was an emotional moment and we were not disappointed. Our host had asked us to guess the vintage whilst he served it from a decanter. He kindly provided us with the solid clue that the year had a '9' in it. We looked at the colour of the wine, we swilled it in our glasses to extract the aromas and bouquet, we were assured it was an original bottle which had never been re-conditioned nor re-corked. The wine showed no signs of its age. There was no apparent oxidation, the colour was not particularly deep but hardly terracotta, and it tasted like a great wine from a vintage fifty years later. Naturally, we were all astounded. It also confounded the theory that wines which are round and approachable early do not age well.

The 'primeurs' or wine futures, whereby wine is sold on behalf of the Bordeaux châteaux by the négociants to merchants around the world, has functioned for centuries, even if it is only in the last 30 years or so that it has gained significant media interest and penetrates into the minds of wine lovers in a way it never did before. For a château, when a particular vintage is offered 'en primeur' – that is to say the 2008 vintage is sold now even though it will not be delivered for another two years - it is hugely important and may make up some 50% or even 75% of its total annual turnover. The quality of the vintage, as perceived by the world at large, is crucial and largely determined by the climatic conditions prevailing.

Any winemaker would have been disappointed by the weather in 2008. Apart from the rather damp and cool conditions in March, which followed a surprisingly warm and sunny start to the year, the frost of April 7th damaged the crop to such a significant degree that some may have suffered a reduction in their harvest of up to 50%, a terrible slice of revenue removed overnight. Perhaps the châteaux worst hit were those of Sauternes, but no less worse affected were those estates in the Graves. Average temperatures in the spring were well down even on last year, and high rainfall in May was not conducive to any real plant growth. Had he had an eye on the financial press with a view to the market he would be offering to in due course, a producer might have been comforted by the Bank of England who were already predicting the end of the global credit crisis and that prices in credit markets, such as US subprime mortgage-backed securities were too low and "overstate the losses that will ultimately be felt by the financial system".

June's weather was not much better than the previous month. Low rainfall in July, however, coupled with good levels of sunshine, brought some optimism to the vinegrower which was rapidly dissipated by the appalling weather in August which continued into the early part of September and mitigated only by the generally late state of the growth of the vines due to the poor weather up until then. At this stage any wine producer might well have thought of throwing in the towel. But towards the middle of September, the sun broke through and ideal conditions reigned for a period long enough to provide the necessary ripening and harvest of the grapes. Even as winemakers saw a light at the end of the tunnel and hoped they would have some wine to sell, Lehman Brothers Holdings filed for bankruptcy protection. Whilst Lehman Brothers bit the dust the US Treasury Department formally asked Congress to approve a $700billion bailout of the financial industry to create a government fund to buy illiquid assets from the nation’s banks and intervened to lend American International Group (AIG) $85billion to try and prevent a global economic meltdown. As the harvest completed, for many châteaux this was two weeks later than normal towards the end of October, the US Federal Reserve cut interest rates by 0.5 percentage points to 1 percent, the lowest level since June 2004, in an attempt to forestall a growing concern that the world's economies were heading into a depression. As the harvest's fruits fermented the US Federal Reserve Board once again cut its benchmark federal funds interest rate from 1 percent to a record low range of zero to one-quarter percent, a bigger than anticipated reduction as alarm grew. The unprecedented action marked the tenth consecutive rate cut since the credit bubble imploded in August of 2007. A stressful year under any circumstances. One full of challenges for the châteaux owners and the overall quality of the wine produced is a further indication (see my article on the 2007 vintage) of the capabilities of winemakers in Bordeaux today.

The backdrop to the presentation and pricing of the 2008 vintage from Bordeaux is this: the US is seeing the fastest economic decline in 26 years including the fastest decline in corporate profits in the last 55 years. What hope then that Bordeaux futures will find a market as governments struggle to sell their own?

Pricing a wine future is essentially an exercise in offer and demand. Around the time of tasting the wines in the spring there is always much discussion about the likely offer price, none more so than this year, 2009, in relation to the vintage on sale, 2008. Obviously, the fundamental motivator for the success of any vintage is its perceived quality. 2008 is, by any standards, a good year for the wines of Bordeaux, notwithstanding the apparently poor weather. This quality is defined by the expression of the grapes from the varieties grown, the quality of the tannins, the fruit and structure of the wine. There are some noble and elegant wines from this vintage, a classic vintage which will produce wines of good aging ability supported by the tannins and acidity. But not all producers will have succeeded during this difficult year, either through lack of investment or perhaps, on a rather more banal level, a despondency at the potential market for their wines. In that sense it is not a great year, not, at least, like the recent vintage of 2005 where most producers were able to produce wines of the highest quality and where the top estates produced outstanding wines.

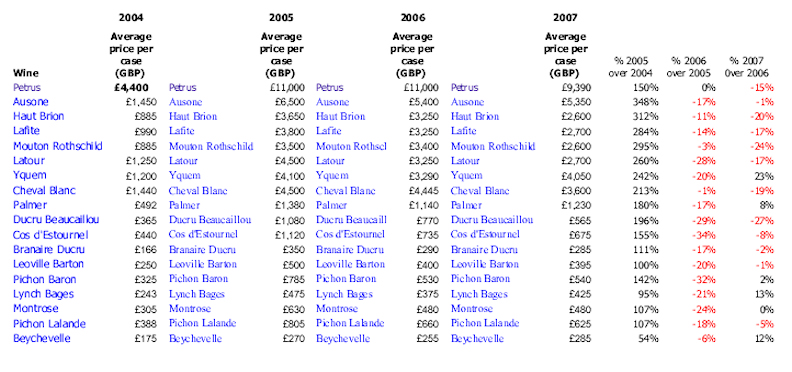

Although the Bordelais are the architects of their own system – a system which is essentially speculative in nature – there has been a growing cry from Bordeaux that speculators are ruining the market by intervening and driving prices up, deterring or even preventing real wine lovers (the wine drinkers) from participating and buying their favourite wines, to drink. Of course, they are right to some extent, but this is the corollary of the system and one which has its parallels in other collectors' markets. In order to counteract some of this effect and because, essentially, the top châteaux were angry that middlemen who had taken little or no risk with a vintage, invested nothing in its quality, but gained significant rewards in the secondary market, raised their prices in 2006 (for the 2005 vintage) to a level which was paradoxically pricing the wines out of the reach of ordinary wine lovers. The ensuing outcry fell on deaf ears as the Bordelais reaped the rewards from the best harvest they had had in years (see Table 1 for release prices on some top châteaux 2004-2007).

Table 1 – Release price evolution 2004 – 2007

The prices set in 2005 were hardly compatible with the refrain from the Bordeaux winemaker that his/her wines were for 'drinking'. But this apparent distaste for the speculator (who, in their eyes are not wine lovers) remains even to the extent that the President of the Union des Grands Crus (a body representing some of the finest wines in Bordeaux) in a recent speech referred, with disdain, to wines which were 'kept on a spreadsheet', it being axiomatic, of course, that these wines were never drunk. A supposition which is hard to support.

![This table gives some idea about the evolution for release prices in the UK for different wines. [Source: wine-searcher.com]](https://finewinemagazine.com/wp-content/uploads/price_jpeg_evolution.jpg)

Whilst basic considerations of price are fairly elemental they are increasingly taking on a complex financial aspect due to the wild fluctuations in exchange rates that have hit the markets in the last couple of years. A cursory glance at the graphs below show just how the Euro has performed against key countries' currencies which means that to supply the UK, for example, at parity to last year, the Place de Bordeaux (the name given to the system in Bordeaux) would need to discount their prices by 30%. Given that the volumes produced are already down by 30%, at least in some cases, this is an almost impossible task. Other currencies have also declined, such as the Korean Won whilst some, such as the US$ and thus the Hong Kong $, have improved.

For the consumer, a decision whether to buy 'en primeur' is based on a number of considerations, not least of which is whether the specific wines might be available later more cheaply or indeed, whether comparable vintages may be available now, which are ready for drinking, and are comparably priced to the 'en primeur' offering. For example, take Château Lynch-Bages, a Cinquième Cru based in Pauillac. Recent auction/retail values on vintages from 1982 to 2004 are as follows (approximate values based on recent auction transactions ore retail offers calculated at on a bottle price at the rate of exchange prevailing at the time of sale): 1982 - $250, 2000 - $200, 2001 - $65, 2002 - $65, 2003 - $65 and 2004 - $60 and 2005 - $95. 2007 is currently trading under its offer price. This would imply that if the release price for this wine is more than the case price for the 2004 of approximately $720 there would be few takers. A similar exercise can be undertaken for any of the other vintages above. Their release price last year was in excess of GBP409 (approx $800+ - the US$ was hovering around $2=GBP1), to maintain parity in the UK market they need to discount this price by 30% (the exchange rate fluctuation since last year) - to GBP290 - so they have a long way to come down. Coupled with a low pound, the economic uncertainty in the market, this is going to be a hard sell to the UK consumer at what would be effectively the same price as last year (assuming they don't discount further), however it would solve the problem of the other vintages sloshing around in the market which are still at a premium, as these wines would then undercut them by almost 50%. Whether price cuts of this kind for 2008 would impact these stocks remains to be seen.

This is not to say that Château Lynch-Bages has been one of those wines which has increased its prices beyond reasonable expectations. Quite the contrary, as can be seen from the table above, despite their attractiveness they have been one of the slowest to increase their prices and one of the fastest to decrease them. On the other hand, speculators have made this a much sought after wine which has shown significant returns in the auction market. This has not been to the disadvantage of the Château when setting their price, especially in the difficult market which prevails today. At the time of writing Château Angelus has lowered its launch price by 40% to Euros70 per bottle (excl VAT). This is only marginally under the UK price for last year.

Rumours abound as to the pricing of these wines this year, and the timetable for their release. According to the sage words of one winemaker's father - "everything that is sold is not for sale" and it has not been considered prudent until now to play the market at its own game. With the prospect of few people taking up the 'en primeur' this year this may be about to change. The big loser this year will be those that bought the 2007 vintage, because whatever happens now, it is effectively 'ruined'. Some merchants are faced with big write-downs. It seems inevitable that there will be some companies which will go out of business, victims of a bubble which the Bordelais were too slow to correct. The paradox is that the 2008 deserves a price well above that of 2007.

Le vent se lève, il faut tenter de vivre...

Fabian Cobb

Bordeaux selections follow.

The Problem with the 2008 is the 2007…

The culture of en Primeur purchasing in the UK is very strong. On the whole, for good reasons; it allows customers to buy at the best price, to have a good chance of securing rare and in demand wines and in the bottle format that is required. They might also benefit from spotting a latent ‘star’ whose true value has not been recognised in the market. These are the compelling en Primeur ideals – I stress ideals.

Bordeaux’s problem is that it is frequently incapable of pricing according to intrinsic quality and market strength. It often uses either one or the other and on the rare occasion it uses both, it usually does so in the wrong way. So it was with 1984 – a bad vintage with a strong US market and therefore grotesquely overpriced. The result? UK Merchants who were forced to buy in order to ‘maintain their allocations’ couldn’t even sell them at cost and they hung around like a bad smell (literally in some cases!) for more than a decade.

Likewise with 1997. A perfectly decent, moderate year priced hugely more expensively than the very good 1995 and 1996. So, a hot market with average quality. The result? See above. Likewise in 2007; a decent year and overpriced. See above again…

In fact, the problem with the about-to-be-offered 2008 is not 2008 itself (likely to be pretty, even very good) but 2007. 2007’s pricing allows significantly less room for manoeuvre on price reductions for a much better vintage (2008) because of the greed shown by most producers with their 2007’s. Factor in the devaluation of Sterling (and the overvalued Euro), a very sticky market and you can appreciate the difficulty.

But it is difficult to weep for the Chateaux owners. They have made a lot of money whilst the Bordeaux négoces and the UK Wine Merchants have had their margins squeezed and squeezed again. The balance has shifted but the consumer has not benefited.

That’s the extent of the problem and, of course, the opportunity. My advice to the Bordelais? Be dramatic, even inspirational. Use 2001 opening prices as a reference, or 2002, or even 2004. You can afford to and you really, really need to make some friends. We all need them in these times do we not?

There are some noble champions of reasonable pricing which is why their wines will sell in any market. Christian Moueix’s prices (in Pomerol and St Emilion) have risen by around 35% – average – in 7 years. Anthony Barton of Chateau Leoville/Langoa Barton has been pretty reasonable. Ditto the lesser Classed Growths who offer fantastic value – Kirwan, Lafon Rochet, St Pierre, Calon Segur, Les Carmes Haut Brion to name a few. It ain’t all bad!

Adam Brett-Smith

Corney & Barrow